If you are an heir to an inheritance, you may wonder how to claim your money and how long it will take to get through the inheritance process. The legal issues surrounding inheritances and estates can be complicated, so understanding the process is essential.

In many cases, heirs are required to wait to receive their inheritance. If you find yourself in this situation and don’t want to wait for your money, you can receive a portion of your money right away with an inheritance cash advance from Inheritance Funding .

Keep reading to learn more about the inheritance process and how to get your inheritance early.

Table of Contents

- What Are the Basic Terms?

- What Is an Inheritance?

- Typical Amount for an Inheritance

- How Does Inheritance Work?

- What Happens When You Receive an Inheritance?

- Tips for Claiming Inheritance

- How Long Does the Probate Process Take?

- How Do I Claim My Inheritance Money Early?

- How Do I Get My Inheritance Cash Advance?

- Get an Inheritance Money Advance With Inheritance Funding Company

What Are the Basic Terms?

There are several basic terms that you may want to familiarize yourself with in anticipation of the inheritance process.

- Estate: An estate refers to the assets a person leaves behind after death.

- Will: A will is a legal document that directs how an owner’s property should be distributed after their death. If there is no will, intestacy laws, which vary by state, determine the distribution of the estate.

- Trust: A trust is a legal document stating how an estate owner’s assets should be distributed to the inheritors.

- Debts: After the owner of the estate dies, their debts must be paid prior to any inheritance being passed to beneficiaries. A beneficiary is not legally responsible for the debts that a relative or parent incurs, but the estate must cover any remaining debts.

- Probate: Probate refers to the legal process during which the property is distributed after the owner’s death. This process is overseen by a court.

- Executor: The executor is the person who is determined in the will or otherwise legally allowed to manage, secure and gather the assets of an estate.

- Estate taxes or inheritance taxes: After the death of the owner, an estate may owe federal or state taxes, known as estate or inheritance taxes. While some taxes may be paid by inheritors, they may also be paid out of the estate’s assets.

What Is an Inheritance?

An inheritance is the assets an individual leaves to their loved ones after they pass away. This inheritance may include more than just cash, such as:

- Stocks and bonds

- Jewelry

- Cars

- Antiques

- Real estate

You may receive inheritance money by being named in a will. In this case, you will go through a probate process to divide the assets. In other cases, assets pass to heirs like a spouse or children. The court appoints an administrator to divide the money and other assets following state laws.

Typical Amount for an Inheritance

About half of all inheritances in the United States are less than $50,000. Transfer amounts change drastically depending on the wealth of the individual who has passed. Transfers of more than $1 million typically happen in about 2% of deaths.

Inheritance amounts ranging from $50,000 to $249,000 account for about 30% of inheritances given. Inheritances ranging from $250,000 to $499,000 make up less than 10% of inheritances. Less than 5% of inheritance recipients receive $500,000 to $1 million in inheritance money.

Some people receive no inheritance, especially if the deceased had a lower income. About 30% to 40% of households receive an inheritance in their lifetime.

How Does Inheritance Work?

When you receive an inheritance, you must go through a process called probate to get the cash and other assets. During this process, the court will review the will, decide each asset’s value and pay bills and taxes. After these steps, the court will distribute the inheritance to loved ones.

The probate process will follow specific laws that vary from state to state. These laws establish the probate steps of the estate and include laws related to intestate succession if a person dies without a will. Even in the case of intestacy, the probate process will include payment of final bills and asset distribution, such as selling property.

Though the laws can vary depending on geographical location, the general steps involved in how to get your inheritance tend to be similar. You can expect the estate to go through the following steps:

1. Authenticate the Last Will and Testament

After the estate owner dies, their will should be filed as soon as possible in the probate court. At the same time, an application or petition to open probate of the estate will be processed. In certain situations, a death certificate may also be needed. To help make the process simpler, state courts provide guidelines and forms for the estate’s executor.

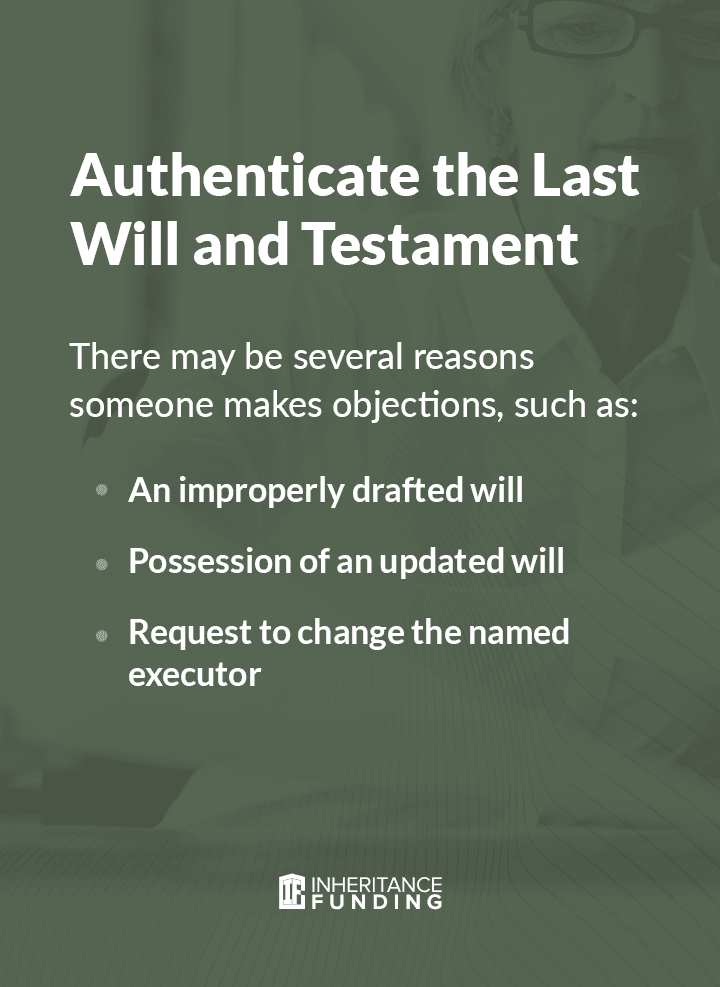

A judge will need to validate the will in a court hearing, and notice will be sent to the inheritors included in the decedent’s will. During this hearing, anyone with concerns has an opportunity to object to the probate process. There may be several reasons someone objects, such as:

- An improperly drafted will

- Possession of an updated will

- Request to change the named executor

To establish a will as valid, the decedent and witnesses should have signed a self-proving affidavit when the last will and testament was signed and witnessed. If the deceased did not create a self-proving affidavit prior to death, additional witnesses can provide sworn statements testifying they saw the decedent sign their last will and testament.

2. Appoint the Executor or Estate Administrator

Next, the judge appoints an estate executor, also known as a personal representative or administrator. This is the person who manages the probate process, including the settling of the estate.

An executor may have been designated in the decedent’s will. If a will doesn’t exist, the court is responsible for appointing an executor, who is typically the next of kin — the decedent’s surviving spouse, or oldest adult child. An individual can choose to decline being appointed as executor. If this occurs, the court will select someone else.

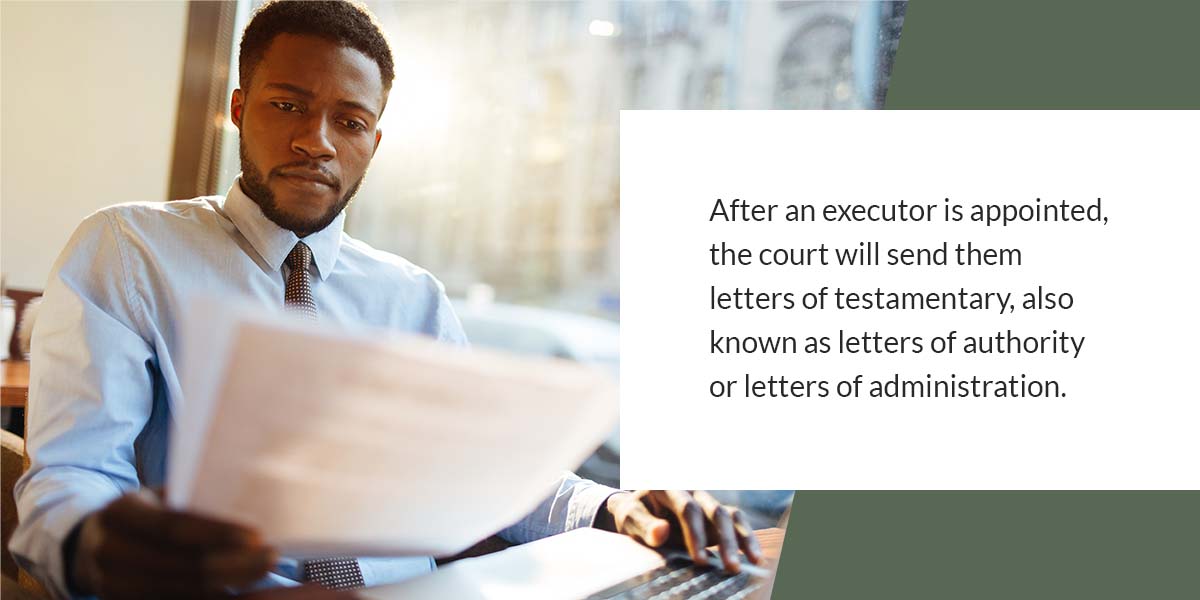

After an executor is appointed, the court will issue letters of testamentary, also known as letters of authority or letters of administration. These legal documents permit the executor to make transactions on the estate’s behalf.

3. Locate the Deceased’s Assets

The executor’s first task is to locate and take possession of assets the deceased left behind to protect them during the probate process. The task of locating assets can be difficult, particularly if there are any the deceased didn’t proclaim. The executor must track down these assets, which can be accomplished by reviewing documentation like insurance policies and tax returns.

Though the executor doesn’t need to move into a property that the decedent owned to provide protection, they should ensure that any mortgages and the associated insurance and taxes are paid to prevent foreclosure. The executor can literally possess other items to store and protect them, such as jewelry, collectibles and vehicles. The documentation for these assets should also be gathered, along with documentation for bank accounts, investment accounts, stocks and bonds.

4. Determine the Date of Death Values

Next, the date of death values for assets should be determined. These values are determined by reviewing account statements and appraisals. In certain states, the court may appoint an appraiser. In other states, the executor may be able to select the appraisers. The executor should provide a legal document that lists each valuable item the deceased left behind. Every asset should have a value and notes that indicate how this value was determined.

5. Inform Creditors of the Death and Pay Debts

The deceased’s creditors need to be notified immediately about the death. Most states require executors to submit a death notice to a local newspaper for publication that can notify the creditors of the estate owner’s passing.

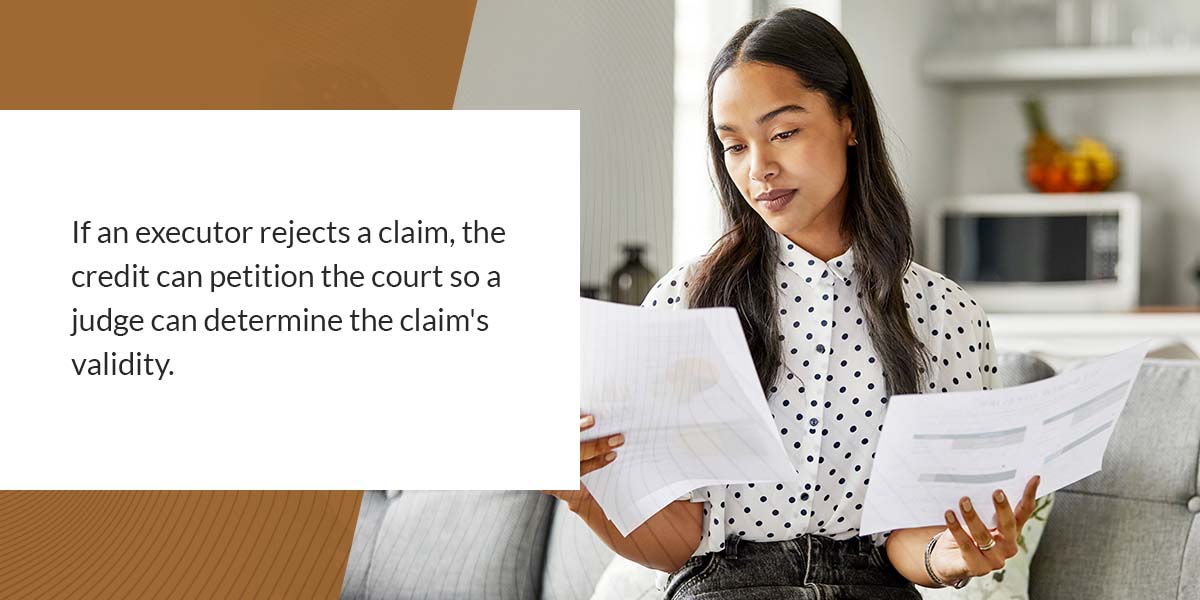

These creditors then have a limited period of time to make claims against the estate. However, the executor can reject these claims if they are believed to be invalid. If an executor rejects a claim, the creditor can petition the court for a judge to determine the claim’s validity.

The executor needs to pay valid claims submitted by creditors using the estate’s funds according to the laws in the state.

6. File the Final Tax Returns

The executor should find out whether the estate is responsible for paying estate taxes. If so, the relevant tax returns should also be filed. The executor can source these payments from estate funds and pay them within an appropriate time after the date of death.

7. Distribute the Estate

Finally, the executor petitions the court for permission to distribute the estate’s remaining assets. The executor will only be permitted to do so after completing the accounting and transactions listed above.

If a minor is one of the beneficiaries or heirs according to the will, the executor needs to prepare a trust, as minors cannot own property. If the heirs are adults, the executor files deeds and transfer documents with the state or county officials to finalize the bequests. At this stage, you receive your full inheritance at last.

What Happens When You Receive an Inheritance?

When you receive an inheritance, you must go through a legal process before you receive the money. The executor submits the will and other documents to the probate court. Any outstanding bills or taxes must be paid before you get the money or other assets in your inheritance. This process often takes several months or even years.

Tips for Claiming Inheritance

If you want to collect your inheritance money, you can take a few steps to make the process simpler. Follow the tips below on how to receive an inheritance without causing yourself unnecessary headaches or stress:

- Stay calm: Try to remain calm throughout the process and avoid making impulse purchases. When you receive your inheritance, this may be the only time you receive a large sum of money or a valuable asset, so you should utilize it carefully.

- Seek expert advice: Seek help from a professional who can give you guidance throughout the inheritance process, such as a lawyer, accountant or financial advisor.

- Document and file records: After the probate process is completed, keep the documents relevant to your inheritance in a safe place. These include the will and trust documents, the death certificate and asset inventory value.

- Keep money in a safe place: Though you have many options for storing your money, you may want to store your inheritance in a certificate of deposit or a low-risk money market fund.

- Consider what the taxes could be: Note that you may have to pay taxes on any inheritance you receive, so you should take that into account when making your plans.

- Determine how much to invest and how much to spend: Put your money to good use by determining how much you want to invest, how much you want to put in savings and how much you want to spend. If you inherited a property, you should also consider what you want to do with this property. Try to make your plans before you receive your inheritance.

When you follow these tips, the process of receiving your inheritance can be smoother and simpler.

How Long Does the Probate Process Take?

To receive your inheritance money after the death of a loved one, you must wait for the probate process to be completed. Since this process is so complicated, you could wait months or even years to receive your money. On average, it takes about 17 months to distribute an estate in the United States. Different factors could delay the process further, such as the will, the estate size, the number of heirs, the probate laws in the state and outstanding taxes or debt.

Will

The probate process can become complicated if the decedent doesn’t have a will. In this case, the court will need to be more involved in each step of the process. Even in the case that the deceased had a will, it may be:

- Non-specific

- Unclear

- Improperly witnessed

- Improperly signed

A will may have been improperly witnessed or signed if it was written under a beneficiary’s influence, the descendent did not have the mental capacity to write a will or fraud was involved in the creation of the will. If these complications arise, a will can be contested and complicate the process of determining who inherits what.

Estate Size

The estate’s size plays a significant role in the probate process. The more assets the estate includes, the lengthier the process will be. Many assets mean more discussions, paperwork and legal decisions.

Calculating the worth of the estate requires that all assets that qualify for probate are evaluated, including real estate, personal property and cash. As a result, the more complex the assets are, the longer this process will take.

Number of Heirs

Similarly, the more heirs there are to an estate, the longer the probate process may take. All of the other heirs to the estate should work together to determine what happens to certain aspects of the estate, such as whether property should be sold. When an estate has several beneficiaries, there are more likely to be disagreements, which can slow or even halt the process.

State Probate Laws

One of the main factors that can slow the probate process is the lack of national regulation. Remember that probate laws vary from state to state, and some states favor a more streamlined probate process than others. Depending on the state the deceased’s estate is in, the process could be lengthy.

Outstanding Taxes or Debt

If the decedent has existing debts or taxes, creditors need to make claims for the money they are owed. It can take months or even years to complete these claims after they’re filed, and the estate can’t close until these claims are resolved.

If the estate owes taxes or is taxable, on the other hand, it can’t be closed until a closing letter is received from the IRS, which can take months after the submission of the tax return and further lengthen the process.

Waiting a long time for the probate process to be completed and receive your inheritance can be frustrating. That’s why we offer inheritance cash advances that give you a portion of your money early.

How Do I Claim My Inheritance Money Early?

How do you get inheritance money before the estate is settled? Inheritance Funding makes claiming inheritance money easy. You can receive a portion of your money early through an inheritance cash advance. We are the oldest, most respected company in the industry, so you can trust that you’ll be getting an advance on your inheritance securely, quickly and at the lowest available price.

How Do I Get My Inheritance Cash Advance?

If you are interested in getting an inheritance cash advance from us at Inheritance Funding, follow the simple steps below:

- Free consultation: First, reach out to us to get a free consultation during which one of our friendly team members will go over the process and pricing and answer any questions you may have.

- Application: To get a portion of your inheritance before the estate is settled, complete an application for a cash advance. At this point, you’ll provide us with documentation proving you’re an heir to the estate. The process for filling out our application is quick and simple.

- Estate review: Next, we’ll review some estate paperwork to make sure the estate has sufficient assets for us to assist you. We’ll begin by reviewing the will, if available, and the petition for probate. We will work with the executor to determine the distribution timeline, which can impact anticipated risks and fees associated with an inheritance.

- Offer: After we write up the terms, you’ll receive an offer. Once we receive your acceptance of the offer, we can move forward with approval.

- Funding: After we confirm the inheritance and approve your application for a cash advance, we can immediately wire the funds to you. We guarantee the fastest service and lowest price available.

- Payout: Once the estate is distributed, we’re paid back out of your share, and you’ll receive the rest of your inheritance.

When you get an inheritance cash advance, you can use your money as you see fit, such as to finance a car, make a mortgage payment, cover medical bills or pay off another existing debt. There’s also no risk to you with an inheritance advance — even if you don’t get any money from the estate, you won’t be responsible for repayment.

We provide our cash advances based on what is in the estate, not on your income, credit score or employment history. There are no monthly payments or hidden fees — all you’ll pay is a flat fee when the estate closes. Additionally, your inheritance cash advance won’t affect the other heirs to the estate.

Get an Inheritance Money Advance With Inheritance Funding Company

Inheritance Funding Company, Inc. (IFC) is the largest provider of inheritance cash advances. Because of the lengthy probate process, as an heir, you could wait for months or years to receive your inheritance money after the death of a loved one. Our inheritance advances allow you to receive a portion of your money the same day you apply for funding to use however you wish.

We guarantee the lowest available price and the fastest and most professional service. We’ll keep your information completely private and secure, so you can rest assured your data will remain safe. Apply now with us at Inheritance Funding to get your inheritance cash today, or contact us for inheritance guidance and to learn more about how to collect your inheritance money.