Losing a parent is a difficult time. If you are an heir to their estate, you may be wondering whether you will be inheriting debt. Generally, most debt in your parent’s name won’t become your responsibility. There are exceptions, such as if you co-signed on a loan. The law prohibits creditors from contacting you to pay off your parent’s debt. Learn more about what happens if your parents die with debt.

Clearing Debts: How Does Inheritance Work When Debt Is Involved?

When a parent passes away, they may leave behind some debt. Generally, you will not inherit debt from your parents when they pass away. Let’s look at the inheritance process when debt is involved.

Can Debt Be Passed Down?

When parents pass away, unfortunately, their debt doesn’t go away. It’s paid off through a process called probate. Creditors have a specific time frame during the probate process when they can file claims against the estate. The executor of the estate will then use its assets to pay off the debt. The assets and property, such as money in a savings account and a home, are part of the estate.

For example, if your parent passes away with cash in their savings account, the estate executor will use these funds to pay off their debt before paying out any money to the heirs.

Can You Inherit Debt From Your Parents?

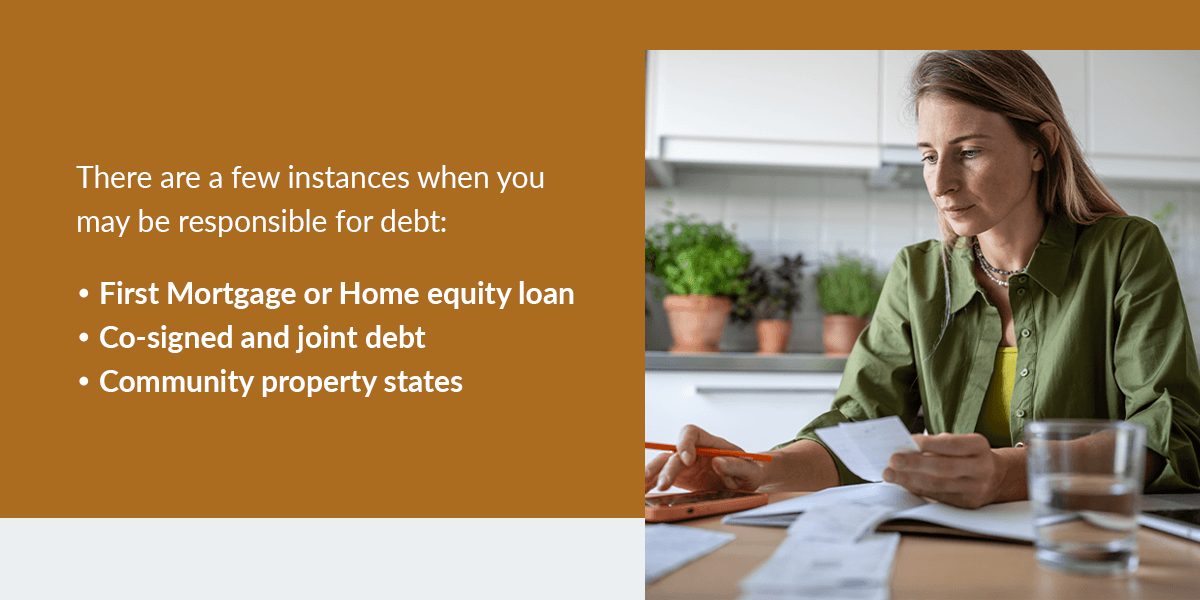

When debt is only in your parent’s name, the estate will pay for it. There are a few instances when you may be responsible for debt:

- First Mortgage or Home equity loan: Inheriting your parent’s home after they pass away can result in debt if they have an outstanding mortgage. You’ll have to continue making the mortgage payments if you want to keep the property. The bank will foreclose on the property if you don’t pay off the debt.

- Co-signed and joint debt: If you and your parent have joint debt such as a credit card or if you co-signed a loan, you’ll have to pay off the balance even if you didn’t use it. This doesn’t apply to authorized users of an account.

- Community property states: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin may have different requirements for a spouse handling their deceased partner’s estate. They may require you to pay some of the debt using community assets, which generally means assets acquired by the couple during their marriage.

Generally, the only debt that is forgiven when someone passes away is federal student debt.

If Your Parents Die With Debt, Who Pays It?

The executor of the estate is responsible for notifying creditors and paying off the debts. They need to produce the death certificate to the creditors and should notify the three credit bureaus so new lines of credit can’t be taken out in their name.

If there are not enough assets in the estate to pay off the debt, the state law will prioritize which debts to pay. You won’t have to pay for any debt in your parent’s name.

The Legal Side of Death: Who Pays off the Deceased’s Debts?

When a loved one passes away, you need to understand the legal side of the deceased’s estate so you don’t get scammed by people posing as creditors.

What Are the Legal Obligations and Protections?

The Fair Debt Collection Practices Act (FDCPA) governs debt collectors and prohibits them from harassing surviving family members to pay off a deceased parent’s estate. They have a designated amount of time to make a claim against the estate. If this time passes, they forfeit the opportunity to receive payment.

Can Creditors and Debt Collectors Approach You?

If a debt collector contacts you, don’t feel pressured to pay immediately. Scammers often exploit people during difficult times and create a false sense of urgency. If you need clarification on the legitimacy of a debt, ask them for proof of the debt in writing. If they are pressuring you over the phone to make a payment, hang up the phone.

Don’t assume that you have to pay. Most debt will come out of the deceased’s estate. Sometimes, a debt collector may contact you, not knowing your loved one is deceased. You can let them know. If they persist in pressuring you to pay the debt, talk to a lawyer who can help protect your assets from debt collectors.

Debt collectors may also contact you to locate the executor of the estate. They aren’t allowed to mention the debt to you, but they may say they’re seeking to identify and locate the person authorized to act on behalf of the deceased person’s estate.

Life After Loss: Navigating Parental Debt and Inheritance Laws

If parents want to preserve their assets, they can take steps to protect them from creditors. Placing the assets in a trust means the assets belong to the trust, not the beneficiaries. This prevents the beneficiaries from spending the assets or creditors from making claims against them.

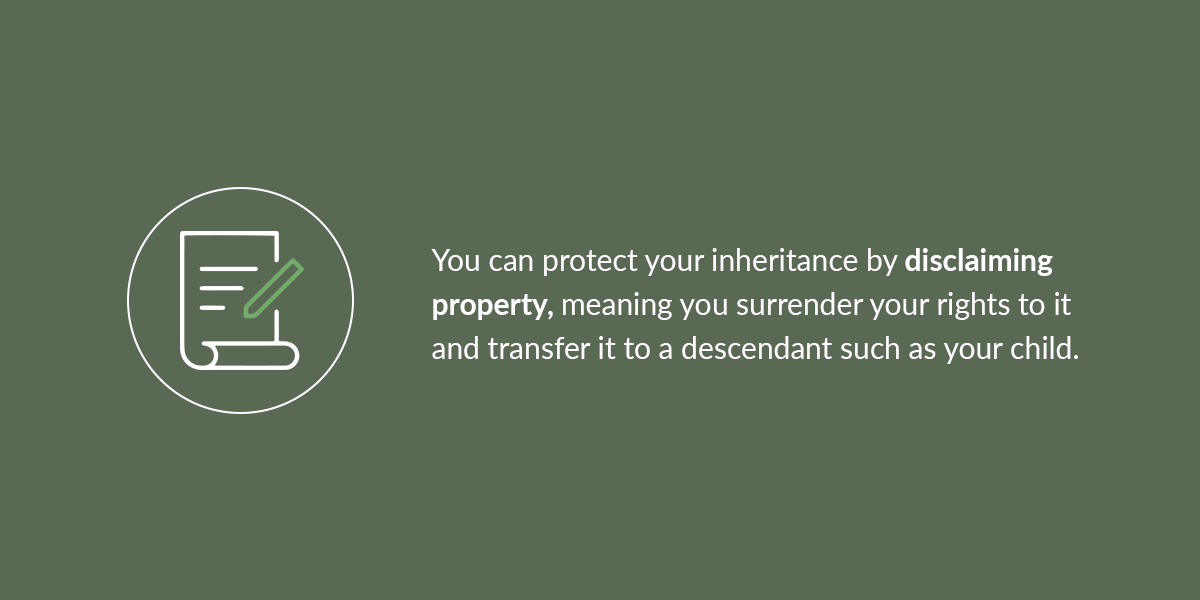

You can protect your inheritance by disclaiming property, meaning you surrender your rights to it and transfer it to a descendant such as your child. You’ll need to disclaim the property before it moves to your name, or a court may claim you committed fraud.

If you live in an inherited home, you may qualify for a homestead exemption, which is awarded to a person using an inherited home as their primary residence. A property that receives this exemption cannot be sold to pay off debt.

A retirement account such as a 401(k), Roth IRA or other retirement investment generally doesn’t go through the probate process, which protects it from creditors. The funds from these accounts go straight to the beneficiaries. If your parent had life insurance and named you as a beneficiary, the money will also go straight to you. It is unlikely that creditors can seize any funds from this policy.

Get an Advance on Your Inheritance With Inheritance Funding

If your parent passes away and leaves a debt, in most cases, this debt will be paid out of the estate. If the debt is solely in your parent’s name, creditors can’t force you to pay it. Scammers tend to take advantage of people during difficult times. If a debt collector does try to pressure you to pay over the phone, it’s best to ignore them. There are only a few instances when you are liable, such as if you have a joint account.

If you have joint debt, you may need money immediately to pay it off. An advance on your inheritance can help to settle debts in your name and cover other urgent expenses. The probate process can be long and drawn out. You can access an inheritance cash advance in as little as 24 hours with Inheritance Funding. To get a quote on your cash advance, contact us today!