If you and your siblings inherit a house after a loved one’s passing and their legal will leaves no directives for how you should use or divide the property, it’s up to your group to choose if you will accept the inheritance and what you will do with the asset. Inheritance is always a complex situation, but it’s much easier to navigate if you and your siblings know what to expect before getting started.

Table of Contents

- You’ve Inherited a House — Now What?

- What Happens When a Mortgaged Property Is Inherited?

- Options When Inheriting a House With Siblings

- Buying Someone Out of an Inherited House

- Options for Inherited Property With Multiple Owners

- IFC Can Help You Get Your Inheritance Money Faster

You’ve Inherited a House — Now What?

Being the beneficiary of a loved one’s house can be overwhelming, especially if you’re simultaneously trying to work your way through the grieving process. Emotions are high, and decisions can be challenging, so the first thing to do is take a step back and allow yourself time and space to deal with what’s happening. After you’ve taken this time, you and your siblings can reapproach the situation with more clarity and confidence.

Consider the following before you get too far into property changes.

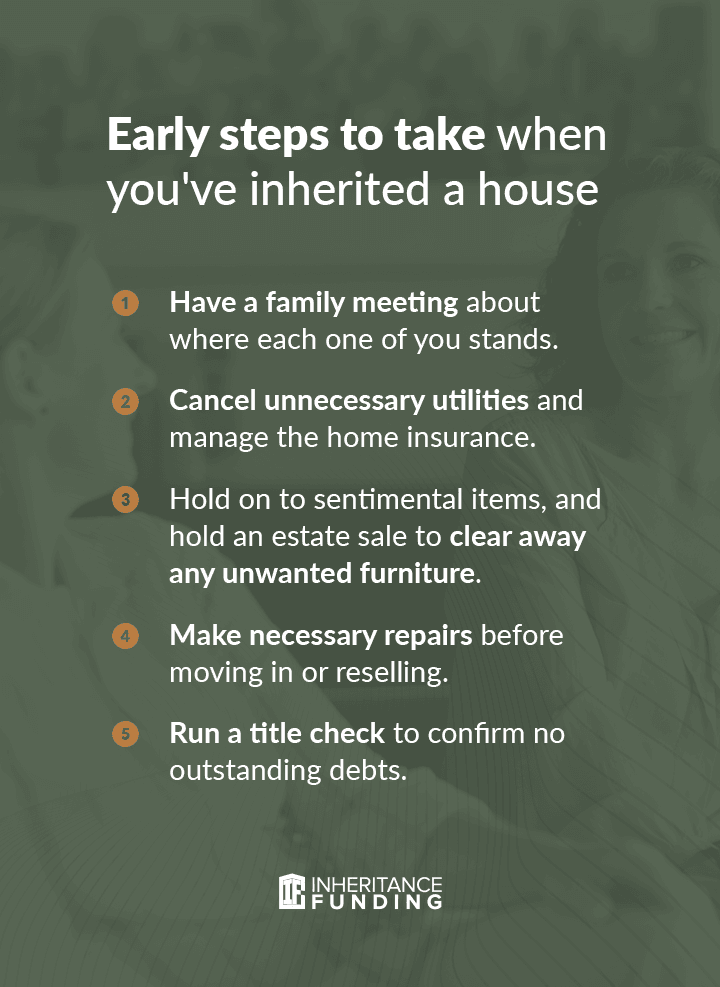

- Have a family meeting: Get together with your siblings and other stakeholders or interested parties. Have an honest conversation about where each beneficiary stands and what they want to happen with the house. Designate different roles for each person — like assigning one person to handle all legal matters and another to take on property renovations — and do your best to collaborate and reach a compromise on any disagreements.

- Manage utilities and insurance: Cancel unnecessary utilities, like streaming entertainment, and transfer any necessities to your or your siblings’ names. Contact the homeowner insurance company and consider whether you’ll seek an alternative insurance plan or transfer the existing policy to your name. Ask your agent about specific timelines and considerations if you plan to sell the house.

- Decide what to do with belongings: Work with your siblings to decide what to do with each remaining item not explicitly mentioned in the will. You may want to hold on to some sentimental items, like family antiques and childhood belongings. Hold an estate sale to clear away any unwanted furniture and use any money to improve the property or split it among siblings and other beneficiaries.

- Make necessary repairs: Inspect the home and assess its current condition, including any water leaks, insulation problems, structural instability or other critical areas you need to repair before moving in or reselling. Consider recruiting a professional to help if damages are extensive.

- Run a title check: Run a title check on the property to confirm no outstanding debts, like unpaid utility bills or liens against the property. If these do exist, bring accounts up to date or work with a lawyer to figure out your next steps.

What to Know About Inheritance Taxes

Inheritance tax is a tax you pay on any inherited asset. Though there is no federal inheritance tax, some states impose it at varying rates.

- Nebraska: Immediate family is typically exempt from inheritance tax up to $40,000, with all others are exempt up to $10,000 or $15,000. The tax rate is either 1%, 13% or 18%.

- Iowa: Immediate family is typically exempt from inheritance tax. For all others, the rate ranges from 5% to 15% of the total inheritance value.

- Kentucky: Immediate family is typically exempt from inheritance tax. All others are exempt up to $500 to $1,000, and the tax slides on a scale based between 4% and 16% plus minimum amounts.

- New Jersey: Immediate family is typically exempt from inheritance tax. For all others, the tax rate ranges from 11% to 16%.

- Pennsylvania: Adult children are exempt up to $3,500 with a 4.5%, 12% or 15% tax rate imposed after.

- Maryland: Immediate family is typically exempt from inheritance tax. Other recipients are exempt up to $1,000 with a 10% tax rate.

What Happens When a Mortgaged Property Is Inherited?

By accepting an inheritance, you and your siblings take on all associated loans, including the mortgage if a property has one. If you and your siblings stand to inherit a house with a mortgage, there are a few options available to you:

- Keep making payments: Inheritors can choose to keep the mortgage under existing terms, maintaining interest rates and the number of payments left. This option can save new owners time and expenses because the mortgage transfers over seamlessly.

- Refinance: If inheritors cannot afford to keep up the mortgage payments, they can seek an affordable refinancing option. This option is especially valuable if the interest rate on the mortgage is higher than the current rates.

- Sell: To avoid liability or payments, inheritors can choose to sell the property or let it go to foreclosure.

Decide with your siblings which option would be most beneficial to you at this time. All options can provide benefits depending on your situation and financial capabilities.

What Is a Quitclaim?

A quitclaim is a document a person can sign to remove their name from a deed and surrender their ownership and interest in a property. It’s a quick way to transfer a title between two parties. They usually work best when both parties know and trust each other since there is a lack of buyer protection.

If a sibling wants to relinquish their ownership of the house they have inherited, they can quickly and efficiently transfer their interest over to another sibling via a quitclaim.

The mortgage is a separate document from the deed, so it’s important to note that it won’t be affected. While the person who signs the quitclaim no longer has ownership, they are still responsible for mortgage payments. If the sibling who owns the property defaults, a lender could force the other sibling to pay if their name also appears on the mortgage.

Options When Inheriting a House With Siblings

In most cases of property passing to multiple owners, each sibling will have an equal share unless stated otherwise in the will. With each party having an equal stake in the property, things can get complicated if you and your sibling disagree about how to use the house. Understanding the dynamics of joint ownership of inherited property is crucial in these scenarios. These are your options when you can and cannot reach an equal compromise.

When You Agree

If you and your siblings agree on how to divide the assets and what to do with the family home, you can establish a personal or private arrangement that dictates how much each person will pay for their portion of the property, how they will pay it, when payments are due and the interest rate, if applicable. Personal arrangements are a good option when no one in your party qualifies for a mortgage from a third-party lender. Anyone uninterested in owning the property can instigate a deed of trust to give the remaining siblings the right to foreclose if they become unable to make their promised payments.

All agreements should be in writing. Ownership options include joint tenancy and tenancy in common. Tenancy in common means you share a title with the property divided either equally or unequally, and each party retains the right to transfer their share to another person with consent from the co-owners. Joint tenancy is when all co-owners have an equal share of the property, and no one can transfer or sell their share without approval from all other co-owners.

When You Disagree

What happens if one person wants to sell an inherited house and the other doesn’t? If you and your siblings cannot reach a compromise, you might have to take your case to court and ask the judge to file a suit for partition, where the judge will terminate your co-ownership and order the property for sale. If you and your siblings are at odds, they may also assign an unbiased third party to help facilitate the property sale.

Should you decide to go this route, you and your siblings will be responsible for paying the third-party referee, as well as any brokers or accountants who help you along the way. Doing so will reduce your profits from the sale and render the property less valuable than if you had sold it on your own without a suit for partition.

Buying Someone Out of an Inherited House

If you or your sibling decide you have no desire to own the property, the interested party can buy the uninterested out of their share of the home. If your sibling does not wish to play a role in future property decisions and wants to grant you full ownership, you need to secure funding to buy their portion of the home. Most third-party lenders won’t give you a loan if the estate has multiple owners, so you’ll need to seek special funding once each co-owner approves of the loan placed against the house. This process typically requires a notice of proposed action and demonstrated ability to refinance into a more conventional loan later.

Determine each sibling’s fair equity by establishing the home’s current value from a third-party appraisal. Subtract the cost of any existing debts or liens, then divide the remaining amount by the number of co-owners. This amount is how much each sibling’s share of the house is worth and how much each person is responsible for paying through cash or loan agreement. Commit all figures and agreements to writing with a legal witness, if possible.

Once you’ve completed the sibling buyout for their share of the property, you’re the official sole owner and may have all documents, utilities, insurance and titles transferred to your name. You can then refinance the home for a long-term mortgage. The process is the same if you’re selling inherited property to a sibling — you’re now free of any associated responsibility.

Using an Inheritance advance to Buy Out Siblings

An inheritance advance is the quickest and most straightforward method to buy someone out of a house. Unlike loans, it gives you immediate access to your assets without waiting for them to close. If you’re inheriting at least $10,000 worth of value from a probate estate, you may qualify for an advance on that amount from Inheritance Funding to help cover the cost of buying out your sibling’s share of the house. This process never affects the estate itself or other co-owners’ shares.

Once we have fully processed the estate and distributed the funds, your amount owed (the amount of your advance, plus our fee) will automatically transfer to us once the estate closes, without any additional work or interest due. If there isn’t enough to cover the cost, Inheritance Funding will take the loss. Learn more about the Inheritance Funding process and how it differs from a loan.

Using an Estate Loan to Buy Out Siblings

Estate loans can let you borrow against a percentage of your inherited property to buy out your siblings from their share of the house. Loan proceeds go to the estate’s account and distribute to interested parties. Once you use your loan to buy out your siblings, they are no longer involved in the process. Estate loans are subject to interest and other fees and may come with strict repayment timelines to consider.

Options for Inherited Property With Multiple Owners

Should you and your siblings decide to take on co-ownership, you can choose to sell the home and split the profits, rent the home out to a new person and split the income equally or keep the house in the family by letting one or more of the siblings move into the home themselves.

Before your family can make the best decision for your inheritance, consider the following:

- The property’s condition

- The cost of any necessary repairs or renovations

- The house’s appraised value

- Where you live

- The current real estate market

- How much time you have to work through the process

- Existing property needs in your family

- Sentimental value

Selling and Splitting the Profits

Selling the house might be the right move for your family if your area’s real estate market is robust. If the house has no mortgage, you’ll have more equity to split among you. Other the other hand, if you need to pay off an existing mortgage or home loan, that will cut into sale profits. You’ll also be responsible for paying commissions, closing costs and real estate fees on any sale You could also choose to sell the home as a sale by owner for more control over the sale. Depending on property type and location, you might also sell the house to a real estate investor as-is for a reduced price.

If the inherited home carries a mortgage that is higher than the current market value, you and your lender should discuss options for a short sale.

Renting and Splitting the Income

Renting the property as a long-term rental or vacation home is a wise option if your family wants to profit from it. As co-owners, you can decide who will manage the property, including maintenance, repairs, upkeep and administrative tasks.

If you’re placing your house on the rental market, consider the 1% rule, which states that the rental should generate 1% of the home’s purchase price each month. If you’re hitting this amount monthly, you should have enough to cover the costs of vacancies and property management.

Keeping the House in the Family

You and your siblings may decide to keep the house in the family by allowing a loved one to move in and become a caretaker or by using it as a vacation home to share throughout the year. If you decide to go in this direction, keep all legal parts of your arrangement in writing, including whose name will be on the title and utilities.

Be sure to consider who is responsible for maintenance and how your family will pay for it as the need arises. Also remember to account for recurring costs like property taxes and homeowner’s insurance.

IFC Can Help You Get Your Inheritance Money Faster

If you recently inherited a loved one’s home, you might be surprised to find out how long it can take to settle the estate. If you’re hoping to sell the house or buy your sibling out of their portion of the property, you may need faster access to the cash you’re entitled to.

At Inheritance Funding, we simplify the process by cutting through all the red tape and endless paperwork and give you a portion of your share instantly — often within the same day! — so you can use it to put toward real estate costs, co-ownership or final expenses. Unlike an estate loan, an inheritance advance from Inheritance Funding has no interest rate and no maximum fee. Plus, if you find you don’t have enough money to cover the costs incurred after finalizing your estate, we’ll take the loss.

As the oldest, largest and most trusted inheritance advance company in the industry, we’re happy to answer any questions you have about our process and what we can do for you. Learn more about IFC and inheritance funding, or request your free quote today!